Water damage is the single most financially destructive condition a home can develop, reducing property value by 5% to 50% depending on severity, location, and how quickly you respond. This isn’t just about repair costs. Water damage triggers structural deterioration, mold growth, appraisal penalties, and financing obstacles that compound long after the water is gone. Understanding why water damage lowers home value gives you the knowledge to act fast, document everything, and protect your equity before it disappears.

Why water damage lowers home value: the real numbers

Water damage reduces home value through two separate mechanisms. The first is physical: rotting wood, weakened foundations, warped flooring, and compromised drywall. The second is financial: buyer hesitation, appraisal deductions, and lender restrictions that shrink your pool of qualified buyers.

The scale of loss depends directly on the type and severity of damage. The table below breaks down how appraisers and buyers typically respond to each category.

| Damage Category | Examples | Typical Value Reduction |

|---|---|---|

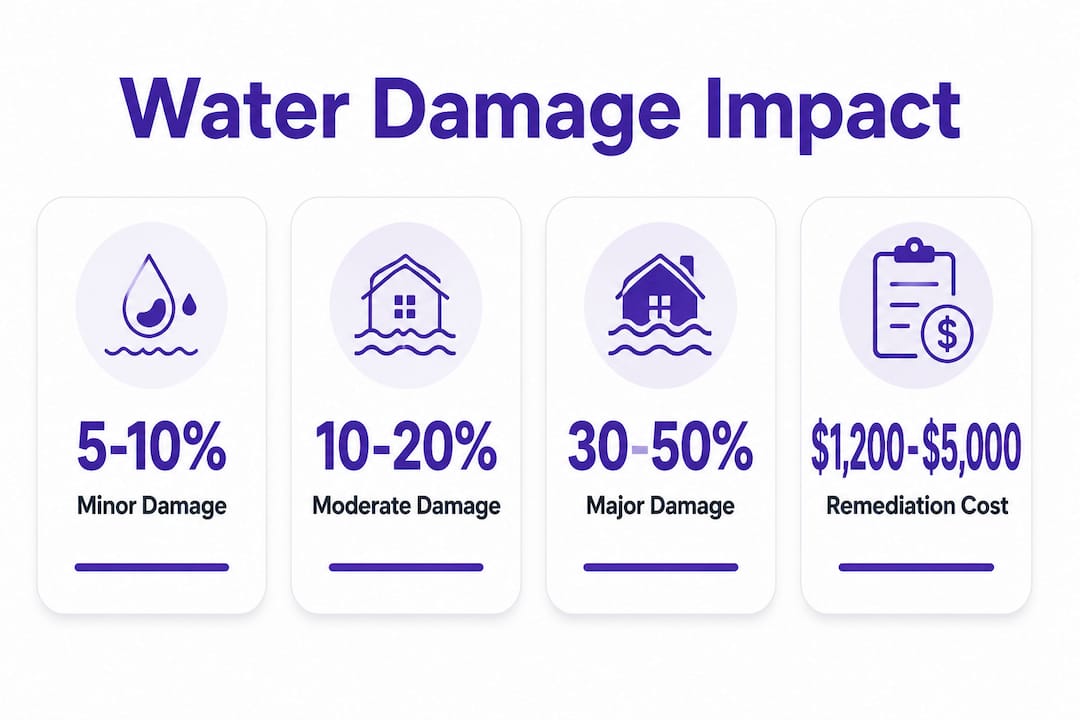

| Minor | Ceiling stains, small leaks, surface discoloration | 5%–10% |

| Moderate | Damp basement, subfloor damage, early mold growth | 10%–20% |

| Major | Structural flooding, extensive mold, foundation compromise | 30%–50% |

Minor damage, like a single ceiling stain from a repaired roof leak, signals a past problem. Buyers discount for the uncertainty of what lies behind the drywall. Moderate damage, such as a chronically wet basement or visible mold on framing, triggers health concerns and structural questions that push value loss into the 10%–20% range. Major structural or flood damage is where the real financial pain lives. Severe water damage causes cash buyers to offer only 50%–70% of after-repair value, meaning you absorb the loss entirely.

The math is stark. A $400,000 home with major unaddressed flood damage could sell for $200,000 to $280,000. That is not a repair cost. That is equity destruction.

Pro Tip: Get a licensed home inspector to assess damage severity before listing. Their written report gives you a baseline for negotiating repair costs and sets realistic pricing expectations.

Does professional remediation recover lost value?

Professional remediation is the most direct way to recover value after water damage. The key word is professional. DIY patches and cosmetic fixes do not recover value. They often destroy it further by giving appraisers and inspectors reason to question what else was handled incorrectly.

Professional remediation costing $1,200 to $5,000 can prevent equity losses of $10,000 to $60,000. That return on investment is difficult to match anywhere in home improvement. The reason is simple: certified repairs eliminate the uncertainty that drives buyer discounts.

What appraisers actually require goes beyond a receipt. Appraisers seek professional remediation invoices, certified mold clearance tests, and engineer certifications to validate repairs. A receipt from a hardware store for drywall compound tells an appraiser nothing. A certified mold clearance report from an IICRC-credentialed firm tells them everything.

Here is what a complete remediation documentation package looks like:

- Remediation invoices from a licensed contractor, itemized by scope of work

- Certified mold clearance test from an independent industrial hygienist, not the same company that did the remediation

- Moisture readings taken before and after drying, showing the structure returned to normal levels

- Engineer’s report for any structural repairs, signed and stamped

- Photographs documenting conditions before, during, and after work

Documented remediation produces significantly less value loss than undocumented or DIY fixes. Appraisers treat undocumented repairs as unresolved problems. That distinction can be worth tens of thousands of dollars at closing.

Pro Tip: Store all remediation documents in a dedicated folder, both physical and digital. Share them proactively with your real estate agent, appraiser, and any buyer’s inspector. Transparency here works in your favor.

What is the stigma factor in water damage appraisals?

The stigma factor is the value reduction applied to a home even after all physical water damage has been fully repaired. This stigma ranges from 10% to 20% and reflects buyer hesitation about problems that may not be visible or documented. It is one of the most misunderstood aspects of how water damage affects property price.

Buyers fear two things above all else: recurrence and hidden damage. A home that flooded once carries the psychological weight of flooding again. Even with a sump pump upgrade and a waterproofed basement, buyers wonder what the seller did not disclose.

Mold compounds this fear dramatically. Mold growth starts within 24–48 hours of trapped moisture. Buyers and their agents know this. The presence of any mold history, even fully remediated, triggers renegotiations or contract cancellations at a rate that surprises most sellers.

The financing layer makes this worse. Consider what happens when a buyer’s lender gets involved:

- The lender orders an independent appraisal that flags water damage history.

- The appraiser applies a stigma deduction on top of repair cost adjustments.

- The lender requires certified proof of remediation before approving the loan.

- FHA and VA loans are frequently refused until moisture and mold issues are fully certified as remediated.

- The buyer’s financing falls through, and you start over with a smaller buyer pool.

Water damage introduces ongoing financial risk affecting insurance, lending, and resale values long after physical repairs end. Historical moisture issues lower condition scoring in appraisal software, which raises ownership cost estimates for buyers. That means even a perfectly repaired home carries a higher perceived cost of ownership, which buyers factor into their offers.

“Lack of transparency is often a bigger threat to home value than the water damage event itself.” — daltxrealestate.com

The practical implication: disclose everything, document everything, and price accordingly. Sellers who try to hide past water damage face legal liability and deal collapse. Sellers who disclose fully and present complete remediation records minimize the stigma deduction.

How to limit the impact of water damage on your home’s value

Speed and documentation are the two variables you control. Everything else, the severity of the damage, the buyer’s risk tolerance, the lender’s requirements, follows from how well you handle those two factors.

Here is what to do at each stage:

Immediately after discovering damage:

- Call a certified water restoration company within hours, not days. Mold growth begins within 24–48 hours, and every hour of delay expands the remediation scope and cost.

- Follow the emergency response steps recommended by restoration professionals to stop the source, document conditions, and begin extraction.

- Contact your insurance company immediately and photograph every affected area before any cleanup begins.

During remediation:

- Hire an IICRC-certified firm. Certification matters to appraisers and lenders.

- Request a written scope of work before any repairs begin.

- Ask for moisture readings at the start and end of the drying process.

Before listing your home:

- Compile your complete documentation package as described in the previous section.

- Disclose all known water damage history in writing, as required by Illinois law and most state disclosure statutes.

- Have a pre-listing inspection done so you know exactly what a buyer’s inspector will find.

Pro Tip: Install a water leak detection system like Moen Flo or Phyn Plus after remediation. These devices monitor flow patterns and alert you to leaks before they become damage. Mentioning this to buyers signals that you take moisture management seriously, which reduces their perceived risk.

Ongoing maintenance matters as much as post-damage response. Gutters cleaned twice a year, grading sloped away from the foundation, and a sump pump with a battery backup are the three most cost-effective protections against the decreasing home value from water issues that most Chicagoland homeowners face.

Key takeaways

Water damage lowers home value through physical deterioration, appraisal stigma, and financing barriers, but professional remediation with complete documentation can recover most of that loss.

| Point | Details |

|---|---|

| Value loss by severity | Minor damage causes 5%–10% loss; major damage causes 30%–50% loss. |

| Remediation ROI | Spending $1,200–$5,000 on certified repairs can prevent $10,000–$60,000 in equity loss. |

| Stigma factor | Even fully repaired homes face an additional 10%–20% appraisal deduction from buyer hesitation. |

| Documentation is critical | Appraisers require invoices, certified mold clearance tests, and engineer reports, not just receipts. |

| Speed reduces total loss | Fast professional response and thorough records can reduce value loss to near zero. |

What 25 years of water damage work taught me about home equity

I have walked through hundreds of homes after floods, burst pipes, and sewage backups across Chicagoland. The homes that recover their value fully are not the ones with the least damage. They are the ones where the owner called us fast and kept every piece of paper we gave them.

The sellers who lose the most are almost never the ones with the worst damage. They are the ones who waited two weeks before calling anyone, then hired a handyman to patch the drywall and paint over it. That approach costs them far more at closing than the original remediation would have. An appraiser who sees fresh paint over a previously wet wall does not see a repair. They see a red flag.

Buyers in the Chicagoland market are sophisticated. Their agents ask about water damage history on every offer. Their inspectors use moisture meters and thermal cameras. You cannot hide a wet basement or a moldy attic from a modern inspection. What you can do is present a complete, certified remediation record that turns a liability into a non-issue.

The financial logic is straightforward. A $3,000 certified remediation job with full documentation preserves $30,000 to $60,000 in equity. That is not a close call. The homeowners I have seen resist professional help to save a few thousand dollars almost always end up losing far more when the buyer’s inspector finds what they missed.

Invest in the repair. Keep the records. Disclose fully. That is the only strategy that consistently protects your equity.

— Jim

Protect your home’s value with Thecleangenius

Water damage does not have to mean permanent equity loss. Thecleangenius has served Chicagoland homeowners for over 25 years, handling floods, burst pipes, sewage backups, and complete property dry-outs with the certified documentation that appraisers and lenders require.

Every job includes the moisture readings, remediation invoices, and certified mold clearance reports that protect your home’s value at resale. Our team is available 24/7 for emergencies across Arlington Heights, Naperville, Schaumburg, Wheaton, and the greater Chicagoland area. When speed and documentation are the two things standing between you and a major equity loss, you need a certified team on site fast. Contact Thecleangenius for emergency water damage restoration or use our restoration company checklist to make a confident hiring decision.

FAQ

How much does water damage reduce home value?

Water damage reduces home value by 5%–10% for minor issues, 10%–20% for moderate damage, and 30%–50% for major structural or flood damage. Severity, location, and remediation quality all affect the final number.

Does fixing water damage restore full home value?

Professional remediation with complete documentation recovers most lost value, but a 10%–20% stigma deduction often persists due to buyer hesitation about recurrence. Full transparency and certified records minimize this reduction.

Can water damage prevent a home sale?

Yes. Lenders including FHA and VA loan programs frequently refuse loan approval until moisture and mold issues are fully certified as remediated. Unresolved water damage can eliminate most of your qualified buyer pool.

How fast does mold start after water damage?

Mold begins growing within 24–48 hours of trapped moisture. This is why immediate professional response is the single most important factor in limiting both physical damage and property value loss.

Does disclosing water damage hurt my sale price?

Disclosure paired with complete remediation records typically produces better outcomes than non-disclosure. Transparency and thorough record-keeping are the most effective tools for retaining value, and hiding known damage creates legal liability that far outweighs any short-term pricing benefit.