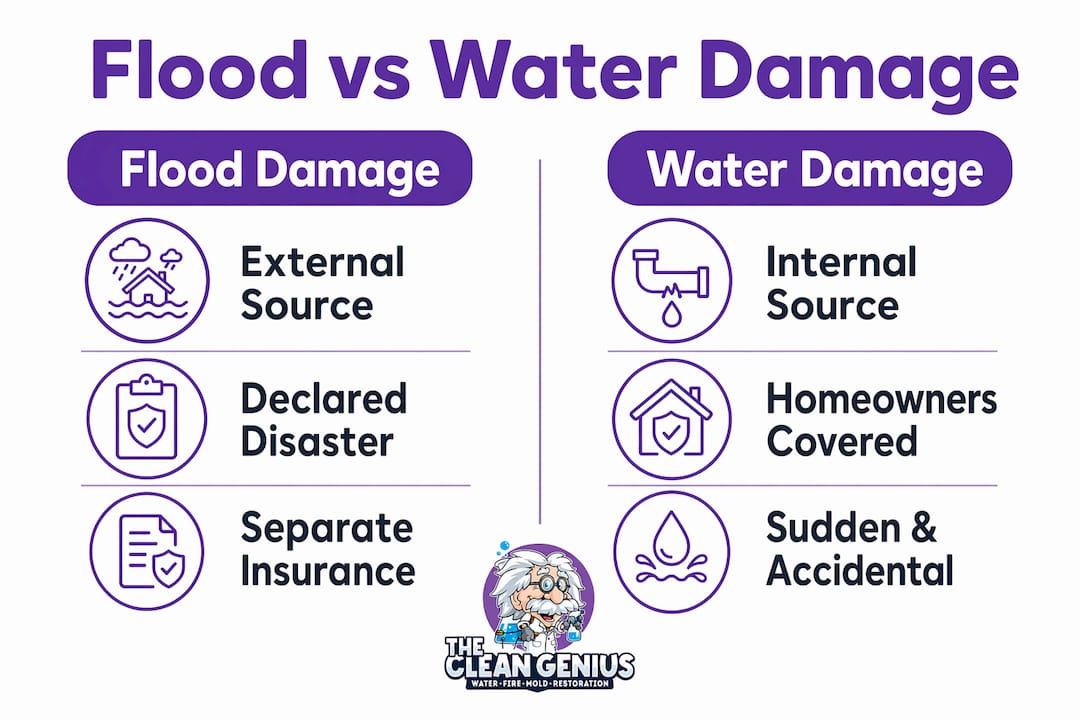

Flood damage is defined as water intrusion caused by external sources, such as overflowing rivers, storm surges, or heavy rainfall, that affects at least two acres of land or two separate properties. Water damage, by contrast, originates inside your home from burst pipes, leaking appliances, or roof failures. Understanding what is flood damage versus water damage is not just a technical distinction. It determines which insurance policy pays, how restoration crews respond, and how much you will spend on repairs. Getting this wrong at claim time is one of the most expensive mistakes a homeowner can make.

What is flood damage versus water damage, and where does each start?

The single most important factor is where the water came from before it entered your home. Flood damage requires external water to impact at least two acres or two separate properties. That threshold is set by the National Flood Insurance Program (NFIP), the federal program that backs most flood insurance policies in the United States. If water from a swollen creek floods your basement and your neighbor’s yard, that qualifies as flood damage under NFIP criteria.

Water damage follows a completely different path. It starts inside the structure, from a pipe that bursts in January, a washing machine hose that fails, or an HVAC drain line that backs up. The water never touches the ground outside. That distinction sounds simple, but it carries enormous financial consequences when you file a claim.

The rule of thumb used by insurance adjusters: water that touches ground outside before entering your home is flood damage, regardless of what caused the storm.

Both types cause serious structural harm. Both can trigger mold growth within 24 to 48 hours. But they are treated as entirely separate events by your insurance company, your restoration crew, and federal regulators.

What causes flood damage, and how is it officially classified?

Flood damage originates from external water sources that overwhelm the ground’s ability to absorb or redirect water. Common sources include:

- Overflowing rivers, lakes, and streams after heavy rainfall

- Storm surges from coastal weather systems

- Rapid snowmelt that saturates the soil and backs up into basements

- Surface water accumulation from prolonged rain that has nowhere to drain

- Municipal stormwater systems that back up into residential areas

The NFIP definition matters because it sets the legal boundary between flood and water damage for insurance purposes. A single flooded basement caused by a backed-up sump pump is not automatically a flood event. The water must have originated externally and affected multiple properties or a significant land area. This is why what is flood versus stormwater damage confuses so many homeowners. Stormwater that enters through a window well during a heavy rain may qualify as flood damage. Stormwater that backs up through your interior drain may be classified differently depending on the entry point.

Flood events are sometimes declared disasters by FEMA, which unlocks additional federal assistance. However, a FEMA disaster declaration does not replace flood insurance. Homeowners without a separate NFIP or private flood policy are left to cover restoration costs out of pocket, even after a declared disaster. That gap surprises homeowners every year across Chicagoland communities like Naperville, Schaumburg, and Elgin, where heavy spring rains regularly push local waterways over their banks.

How does water damage differ in cause and typical scenarios?

Water damage originates inside the home and is typically caused by sudden, accidental events. The most common sources are:

- Burst or frozen pipes during cold winters, which release large volumes of water quickly

- Leaking or failed appliances such as dishwashers, refrigerators with ice makers, or water heaters

- HVAC condensate line failures that allow water to pool in ceilings or walls

- Roof leaks that allow rain to enter through damaged shingles or flashing

- Toilet or sink overflows from clogs or mechanical failures

The origin point matters for restoration too. Water from an overhead source, like a roof leak or a burst pipe in the ceiling, travels downward and saturates insulation, drywall, and flooring before you notice it. Water from a ground-level source, like a washing machine overflow, spreads horizontally across floors and under cabinets.

Standard homeowners insurance covers sudden and accidental water damage in most cases. The key phrase is “sudden and accidental.” A pipe that bursts overnight qualifies. A slow drip under the sink that you ignored for six months does not. Neglected maintenance voids coverage because insurers classify it as wear and tear, not an accident.

Pro Tip: Take photos of your plumbing, roof condition, and appliances once a year. Dated photos prove your home was properly maintained if an insurer questions whether damage was sudden or the result of neglect.

How do insurance policies treat flood damage versus water damage?

The coverage gap between flood and water damage is one of the most misunderstood areas in homeowner insurance. Here is how the two types are treated:

| Coverage type | Water damage | Flood damage |

|---|---|---|

| Standard homeowners policy | Covered if sudden and accidental | Not covered |

| NFIP flood insurance | Not applicable | Covers structure and contents up to policy limits |

| Private flood insurance | Not applicable | Available as supplement or alternative to NFIP |

| Wear and tear or neglect | Excluded | Excluded |

FEMA confirms that standard home policies exclude flood damage entirely. Flood coverage must be purchased as a separate policy, either through the NFIP or a private insurer. Many homeowners in Chicagoland assume their standard policy covers everything water-related. It does not.

Claim denials often happen because homeowners mislabel the origin of the damage. If you call a roof leak “flooding,” your adjuster may route the claim to your flood policy, which does not cover roof leaks. If you call a basement flood from a storm surge “water damage,” your standard policy will deny it. Insurance adjusters determine coverage by tracing the exact path water took before entering your home. Clear documentation of that path is the difference between a paid claim and a denial.

Pro Tip: When you document water damage for insurance, photograph the water entry point, the affected rooms, and any visible external conditions like standing water in the yard. Timestamp everything.

What are the differences in restoration costs and approaches?

Restoration scope and cost depend heavily on two factors: the source of the water and its contamination level. Water is classified into three categories that drive the entire remediation process.

Category 1 (clean water) comes from a supply line or rain entering through a roof. It poses no immediate health risk. Restoration focuses on extraction and drying.

Category 2 (gray water) comes from appliances like dishwashers or washing machines. It contains contaminants that can cause illness. Porous materials like carpet padding often require removal.

Category 3 (black water) includes sewage backups and floodwater. Black water restoration requires full containment and disposal of all porous materials. It costs two to four times more than clean water remediation. Floodwater almost always qualifies as Category 3 because it carries soil, bacteria, and chemical runoff from streets and yards.

On the cost side, professional water damage restoration averages $3,867, with a typical range of $1,384 to $6,384. Severe Category 3 incidents, including most flood events, regularly exceed $25,000. That gap reflects the difference between drying out a burst pipe in a bathroom versus gutting a flooded basement down to the studs.

Rapid response is the single biggest cost control lever available to you. Delaying mitigation by 48 hours typically turns a repairable project into a full reconstruction. Mold begins colonizing wet materials within 24 hours. Drywall that could have been dried in place becomes a tear-out job. Hardwood floors that might have been saved begin to warp and buckle. You can learn more about that specific risk in this guide on warped floors from water exposure.

Professional moisture testing costs $200–$500 and is not optional. Skipping it risks sealing moisture inside walls, which leads to mold growth and can double your total restoration budget. Thecleangenius uses professional moisture testing on every job to confirm complete drying before any reconstruction begins.

The Illinois restoration cost factors that drive prices up most are water category, square footage affected, and how long the water sat before mitigation started. Controlling that last variable is entirely within your power.

Key Takeaways

Flood damage and water damage are legally and practically distinct events. Knowing the difference protects your insurance claim, your wallet, and your home.

| Point | Details |

|---|---|

| Origin defines the type | Flood damage comes from external sources; water damage starts inside the home. |

| Insurance coverage differs | Standard policies cover sudden water damage; flood damage requires a separate NFIP or private policy. |

| Water category drives cost | Black water events cost two to four times more than clean water remediation. |

| Speed controls damage | Delaying mitigation by 48 hours often converts a repair into a full reconstruction. |

| Documentation wins claims | Photographing the water entry point and path prevents claim denial from misclassification. |

What I’ve learned after seeing hundreds of water and flood claims go wrong

After working alongside homeowners through countless water and flood events across Chicagoland, the mistake I see most often is not the damage itself. It is the assumption that all water damage is the same.

Homeowners call me after a heavy rain and say, “We have flooding.” Then I ask where the water came from, and it turns out a roof vent failed. That is not flood damage. That is a covered water damage claim. The wrong label on the first call to their insurer already created a problem. Knowing the exact origin of the water before you call your insurance company is the most valuable thing you can do in the first hour after an event.

The second mistake I see is waiting. I understand the instinct to assess the situation, call family, and figure out next steps. But water does not wait. Every hour matters. The 24-hour response window is real. I have seen homeowners save tens of thousands of dollars simply by calling for professional mitigation the same night the damage happened.

The third mistake is skipping the moisture test at the end of the job. Some homeowners see dry walls and assume the job is done. Moisture hides inside wall cavities, under subfloors, and behind baseboards. Sealing that moisture in is how a $4,000 restoration becomes a $15,000 mold remediation six months later.

My advice: review your insurance policies today, before anything happens. Confirm whether you have flood coverage. If you live near a drainage basin, a low-lying street, or anywhere in the Chicago suburbs that sees heavy spring rain, a separate flood policy is worth the cost.

— Jim

Thecleangenius is ready when water damage strikes

When water enters your home, the clock starts immediately. Thecleangenius provides 24/7 emergency water damage restoration in Chicagoland for homeowners across Arlington Heights, Naperville, Schaumburg, Elgin, and the surrounding suburbs.

Our certified team handles the full process: water extraction, structural drying, moisture testing, and insurance documentation support. We work directly with your insurance company and know exactly how to classify flood versus water damage events to support your claim. With over 25 years of combined experience and more than 400 five-star reviews, Thecleangenius gives you a fast, professional response when you need it most. Call us any time, day or night.

FAQ

What is the main difference between flood and water damage?

Flood damage originates from external water sources affecting at least two acres or two properties, as defined by the NFIP. Water damage starts inside the home from plumbing failures, appliance leaks, or roof breaches.

Does homeowners insurance cover flood damage?

Standard homeowners insurance does not cover flood damage. Flood coverage requires a separate policy through the NFIP or a private flood insurer.

How do I know if my basement water is flood damage or water damage?

If the water entered from outside, such as through a window well, foundation crack, or storm drain backup, and affected neighboring properties, it is likely flood damage. If it came from a burst pipe or failed sump pump with no external flooding, it is water damage.

How much does flood damage restoration cost compared to water damage?

Professional water damage restoration averages $3,867 for typical incidents. Severe flood events, which involve Category 3 black water, regularly exceed $25,000 due to full containment requirements and structural material disposal.

How quickly should I respond to water or flood damage?

Respond within 24 hours. Delaying mitigation by 48 hours typically escalates a repairable project into full reconstruction and significantly increases the risk of mold growth.